Product Category

- Clean Room

- HVAC System

- Water for Pharmaceutical Use

- Sanitary Distribution Piping

- Solution Formulation System

- CIP/SIP System

- Control System

- Tablet Production

- Capsule Production

- Powder Vial Production

- Liquid Vial Production

- Oral Liquid Production

- Eye Drop Production

- IV Solution Production

- Cream/Ointment Production

- Soft Gelatin Production

- Pilot Production

- Ampoule Production

News & Events

Current position: Home >

News & Events

Rethinking the Future-New Business Models for Pharma

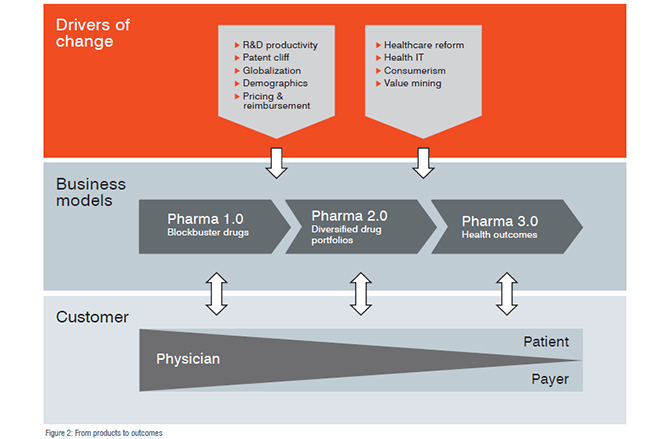

In countries around the world, healthcare spending continues to grow at an unsustainable rate. As a result, a growing priority for governments today is increasing the effectiveness of their healthcare systems. Many countries, from the US, parts of Europe and Japan to fast-growing markets such as China and India, have made healthcare reform a top priority.

Initially, the primary objective of most healthcare reforms has been to contain costs. But, more recently, policymakers have taken new initiatives to improve the sustainability of healthcare systems, looking beyond cost considerations to population health.

Spending on drugs has been a highly visible target for cost containment. But, as it weathers short-term cost-cutting initiatives, the pharmaceutical sector is being presented with clear opportunities to prove that it is able to bring value to healthcare systems.

The fundamentals of the pharmaceutical industry are strong. In most countries, years of better care and nutrition have led to ageing populations, expanding the potential patient base. Meanwhile, rising incomes in emerging countries are boosting demand for higher-quality healthcare. These trends are underpinned by an ongoing surge in the prevalence of chronic diseases, such as cancer, diabetes and heart disease, which require long-term treatment.

But pricing and regulatory challenges, among others, have put the industry’s traditional business model‘Pharma 1.0’, if you likeunder tremendous pressure. As a result, it is being forced to become more innovative, collaborative, diversified, global and value-driven. Today, most pharmaceutical companies are in the process of transforming their businesses along these ‘Pharma 2.0’ lines. This transformation has an impact on all aspects of pharma companies’ operations.

Pharma 3.0

Just as the industry began to embark on its Pharma 2.0 journey, new and sweeping trends are again transforming the business environment. Changing incentives are reshaping the healthcare ecosystem, as policymakers realise that in a sustainable value proposition, health outcomes are the most valuable currency. This shift will, in turn, require the pharma industry to also develop business models focused on health outcomes, where the traditional product a drugis only one part of pharma’s value proposition.

Just as the industry began to embark on its Pharma 2.0 journey, new and sweeping trends are again transforming the business environment. Changing incentives are reshaping the healthcare ecosystem, as policymakers realise that in a sustainable value proposition, health outcomes are the most valuable currency. This shift will, in turn, require the pharma industry to also develop business models focused on health outcomes, where the traditional product a drugis only one part of pharma’s value proposition.

Health outcomes

In an outcomes-focused healthcare system, stakeholders will be rewarded for the perceived value they deliver to the system. Information technology is a major enabler of this kind of approach. Digitalised health data, electronic health records and associated platforms offer the promise of enhancing efficiency, increasing safety and reducing costs. Mobile health technologies provide live and real-time access to health information, supporting diagnosis and monitoring, as well as driving compliance in medication.

In an outcomes-focused healthcare system, stakeholders will be rewarded for the perceived value they deliver to the system. Information technology is a major enabler of this kind of approach. Digitalised health data, electronic health records and associated platforms offer the promise of enhancing efficiency, increasing safety and reducing costs. Mobile health technologies provide live and real-time access to health information, supporting diagnosis and monitoring, as well as driving compliance in medication.

.jpg)

This tremendous expansion of availability of health data is empowering payers to implement outcomes-based pricing and reimbursement. The same transformation is happening on the patient side. The convergence of social media and health information means that we are empowered to improve our health, with access to information that, in the past, was available only to our physicians. Traditional patients are becoming ‘super consumers,’ capable of making real, value-based decisions based on their health outcomes.

These shifts are attracting many non-traditional players, including e-health and mobile health firms, consumer electronics companies, large retailers, medical technology firms and information aggregators. At EY, we recently surveyed business development and innovation leaders and found overwhelming agreement that these new entrants will play an increasingly important role in the health outcomes ecosystem.

What can pharma do to prove its value in this new, complex environment? If it is to deliver on health outcomes, it will have to engage in the cycle of care around the patient, from predisposition testing, prevention, diagnosis and therapy to patient monitoring. The industry’s 2.0 business model is not equipped to deliver on such a value proposition. To move to 3.0, it will need to collaborate with non-traditional players and co-create value for patients, payers, governments and business partners. Pharma companies seeking to deliver health status improvements need to reach new patients by tackling underserved markets, meet unmet medical needs and do a better job of serving existing patients by managing patient outcomes. Their business models will need to combine three core value propositions:

· Managing patient outcomes by, for example, fostering compliance through patient engagement, or engaging in healthcare delivery either directly or by enabling a more targeted delivery through patient population stratification.

· Expanding access to healthcare in underserved markets, in developing countries and in more mature markets for uninsured patient populations. Examples of collaborations to expand access include partnerships between pharmaceutical companies, governments and/or non-profit organisations.

· Meeting unmet medical needs in complex indications such as oncology or immunology as well as in underserved therapeutic fields such as malaria, dengue fever and orphan diseases.

Business model innovation

We have found that pharma executives understand the new business environment, but there is resistance to adapting business models to suit. Three main challenges have emerged in our conversations:

We have found that pharma executives understand the new business environment, but there is resistance to adapting business models to suit. Three main challenges have emerged in our conversations:

· The current business model is working. It is still delivering high margins and solid growth in its current configuration and is expected to continue to do so in the short or mid-term.

· The industry will need to explore uncharted territories to develop business models around health outcomes. Companies will need to develop partnerships with players from other industries, which are beyond their current comfort zone.

· The ecosystem is changing too quickly for pharma to respond. The industry’s product development lifecycle is notoriously long. In the new ecosystem, the business environment is rapidly evolving, as new technologies appear almost daily.

These are all valid obstacles to change. But the industry can overcome them by taking a ‘commercial trial’ approach, leveraging and reimagining some of the things they do best. Many of these initiatives are now under way at all levels of the industry.

· Pilots: Once a company has identified a strategic area on which it wants to focus, its next step should be to identify different ways in which it can play in that space and to test those in early pilot versions.

· Rapid prototyping: Succeeding in the future will mean ending failing experiments and leveraging lessons learned through rapid prototyping. This will require new cultural mindsets that provide incentives for speed, flexibility and experimentation.

· Open innovation: Delivering new outcome-based products and services will require combinations of competencies that no firm possesses in-house. Companies will need to bring an outside-in, open approach.

· Flexible contro: Alliances will need to be sufficiently well-defined to maintain the focus of the collaboration but flexible enough to allow for quick response to new challenges and opportunities.

· Portfolio management: Companies will need to look across their alliance portfolios so that partners can learn from each other, identify synergies and increase the overall value they deliver.

Pharma 3.0 represents a significant shift from Pharma 2.0’s ‘contractual’ collaborative approach, where pharma companies have been in the driver’s seat in managing collaborations with business partners and controlling and commercialising most of the value creation. So to succeed in Pharma 3.0, companies will need to step outside the familiar and relinquish control, combining capabilities, resources, channels and customer relationships with those of their business partners.

The life sciences industry is already good at traditional R&D collaborations with peers or biotech. Partnering with non-traditional players from other industries, such as technology, insurance, internet services, food and retail, may require assimilating a host of differences in operations and cultures.

Source: PharmaFocusAsia